At Pilarski Real Estate Group, our commitment is to provide our clients with sophisticated, data-driven market insights. We believe that clarity is the foundation of confidence, especially when navigating the complexities of high-value real estate transactions in Toronto.

Understanding the legislative landscape is critical to formulating an effective real estate strategy. Today, we are providing essential analysis regarding an important update to the Toronto Municipal Land Transfer Tax (MLTT) specifically targeting the luxury market sector.

The Context: A Shift in Luxury Taxation

In response to evolving fiscal requirements, the City of Toronto has implemented a new, graduated tax structure for high-value residential properties. While the concept of a “luxury tax” is not new, this adjustment represents a significant shift in the calculation of closing costs for properties meeting specific value thresholds.

The primary objective of this measure is to introduce greater progressivity into the tax system, ensuring that investments at the highest end of the market contribute proportionally to the city’s infrastructure and services.

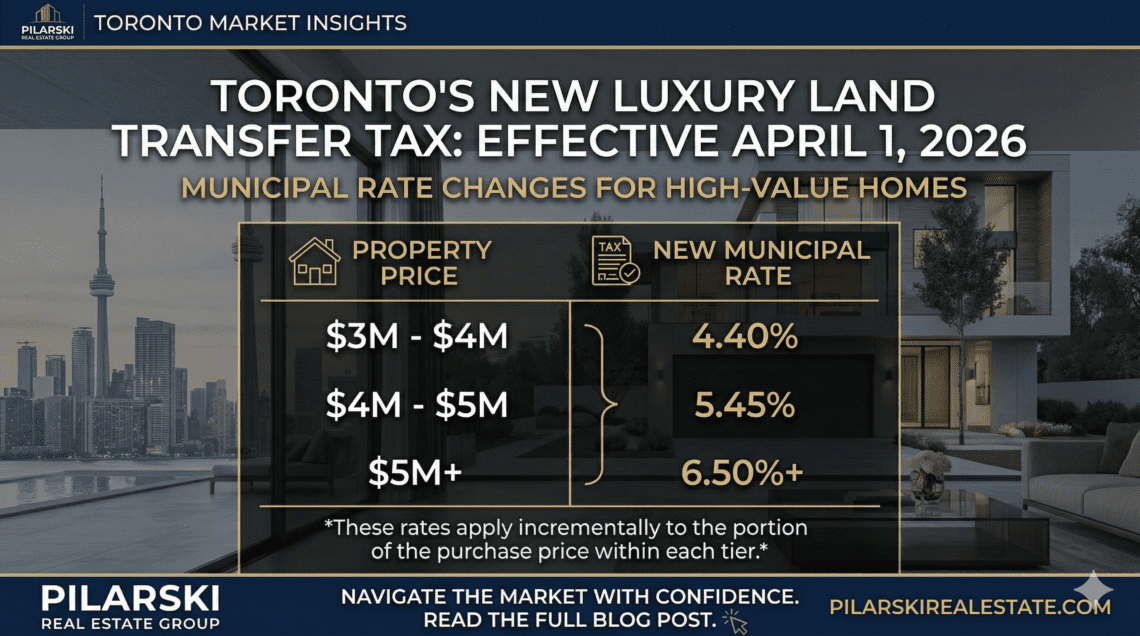

The Specifics: The New Graduated Tiers

Effective April 1, 2026, the new MLTT rates follow a graduated structure. It is important to note that these rates are marginal; they apply only to the portion of the property value that falls within each specific band.

The new tiers apply as follows:

- Properties up to $3,000,000: The existing tax structure remains unchanged.

- The portion between $3,000,000 and $4,000,000: A new rate of 4.40% applies to this specific band.

- The portion between $4,000,000 and $5,000,000: A rate of 5.45% applies to this specific band.

- The portion above $5,000,000: A rate of 6.50% applies to any value exceeding this threshold.

What This Means for Your Next Transaction

For clients considering transactions in the luxury sector, this adjustment directly impacts the “cash to close” required upon settlement.

For illustrative purposes, consider the acquisition of a property valued at $5,000,000. Under the previous structure, the municipal tax would have been a flat percentage. Under the new graduated system, the tax is calculated incrementally:

- Standard MLTT on the first $3M.

- 4.40% on the $1M band between $3M and $4M ($44,000).

- 5.45% on the $1M band between $4M and $5M ($54,500).

This results in a total MLTT obligation that is perceptibly higher than under the previous model. When combined with the Provincial Land Transfer Tax, the total acquisition cost must be carefully factored into your financial planning.

Our Strategic Perspective

At Pilarski Real Estate Group, we view this legislative update as another variable to manage, rather than an impediment.

- For Buyers: Precision in financial planning is paramount. Accurate projections of all closing costs, including the new graduated MLTT, are essential before making an offer on a high-value home.

- For Sellers: Understanding the tax implications for potential buyers is key to realistic pricing and negotiation strategies. Properties positioned near the tax thresholds may require specific approaches to maintain maximum market appeal.

The Toronto market remains robust, fueled by strong demand and limited supply in premier neighborhoods. While tax adjustments introduce new calculations, the fundamental value of prime Toronto real estate endures.

Partner with Pilarski for Expert Guidance

We are dedicated to providing the high-level expertise required to navigate these changes seamlessly. Our team is prepared to analyze your specific real estate goals and ensure your portfolio strategy is optimized for the current regulatory environment.

Should you have any questions regarding how these Land Transfer Tax adjustments may impact your upcoming real estate plans, please contact us for a confidential consultation.